Discover the "Beat The Bank" Home Loan Strategy

That Can Slash Years and Interest Dollars Off Your Mortgage… Without Increasing Your Monthly Payment

Watch this short explainer to see why a typical 30-year loan on a $300k–$400k home can secretly cost you up to 140% of what you borrowed in interest alone—and how a different loan structure can help you pay off your home in as little as 3–10 years instead of 30.

Click to Watch Explainer Video

Secure & Confidential

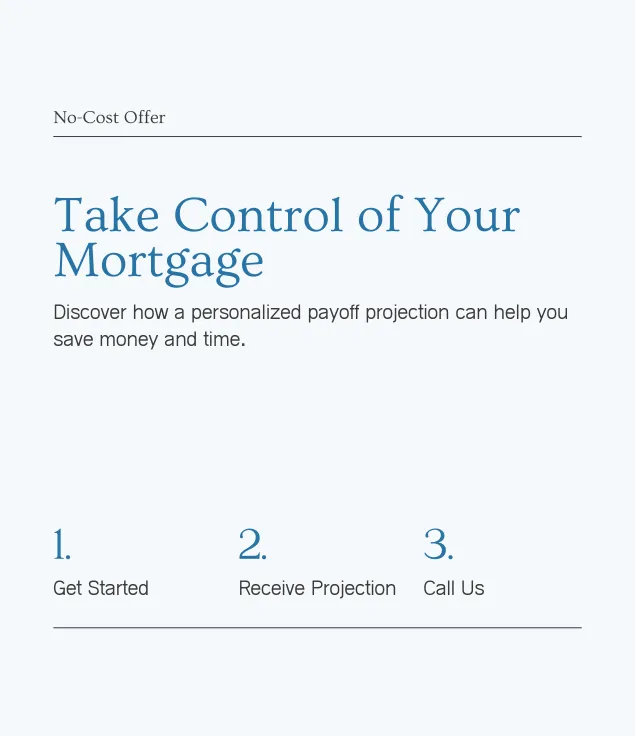

5-Minute Analysis

No Cost, No Obligation